You’ve landed your first real job, congratulations! That first paycheck feels empowering, doesn’t it?

But before you rush off to buy that long-awaited phone or treat your friends, here’s the truth: how you manage your money in this first year can shape your financial future for decades. Many young professionals start strong with ambition and dreams, but soon find themselves overwhelmed by bills, poor choices, or unplanned emergencies. The good news? It doesn’t have to be that way.

In this article, we’ll walk you through seven practical and biblically grounded financial tips to help you build a solid foundation in your first year of employment.

You’ll learn:

- Budget Wisely Without Feeling Restricted

- Start Small with Savings and Build Consistency

- Build an Emergency Fund to Stay Financially Prepared

- Tithe and Practice Generosity to Strengthen Your Financial Health

- Avoid Debt Traps and Credit Card Temptations

- Set Long-Term Financial Goals and Start Planning Early

- Stay Motivated with Faith-Aligned Money Goals

- Conclusion

Ready to take control of your money and align it with your values from day one? Let’s explore these seven smart money moves and set your financial journey on the right track.

Budget Wisely Without Feeling Restricted

One of the most essential money management tips you can apply in your first year of employment is learning how to budget wisely.

Your income may seem substantial at first—especially compared to what you were accustomed to as a student or job seeker—but without a clear plan for your expenses, it’s easy to lose track and overspend.

Start by creating a monthly budget that includes your bills, savings goals, debt repayment, and personal spending. Use the 50/30/20 rule as a guide: allocate 50% of your income to needs (such as rent and groceries), 30% to wants (things you can live without but add comfort to life, like entertainment), and 20% to savings and debt repayment.

Having a budget doesn’t mean you can’t enjoy your money. It means you’re telling your money where to go, rather than wondering where it went.

Tweet

Scripture makes it clear:

"The plans of the diligent lead surely to plenty, but those of everyone who is hasty, surely to poverty" ( Proverbs 21:5, NKJV).

Now that you’ve laid the groundwork with a solid budget, let’s explore why starting small with savings can yield significant benefits down the road.

Start Small with Savings and Build Consistency

Don’t wait until you’re earning more to begin saving.

Start early and start small. Open a savings account (preferably one with high-interest rates) and commit to setting aside a percentage of your income every month. Even 5% can make a difference over time.

Consider setting up automated transfers to your savings account so that saving becomes effortless. This helps you stay consistent, even when other demands come up. Building this habit early lays the foundation for financial independence and peace of mind.

Your savings should be divided into short-term and long-term buckets. Your short-term savings can cover expenses such as travel or new gadgets. Your long-term financial goals might include investments, a home, or even retirement accounts.

But what about life’s unexpected twists? That’s where an emergency fund comes in.

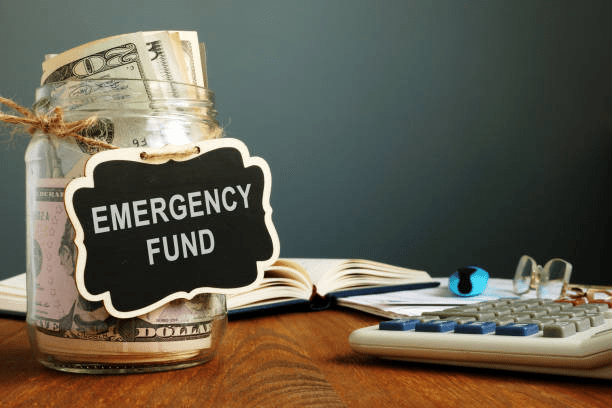

Build an Emergency Fund to Stay Financially Prepared

Life can be unpredictable.

An unexpected job loss, medical emergency, or car repair can quickly drain your account if you’re not prepared. That’s why one of the smartest money moves is to build an emergency fund.

Aim to save at least 3 to 6 months’ worth of essential expenses. Keep this money in a separate, easily accessible account, and only use it for real emergencies. This isn’t your backup for online shopping or impulse buys!

Having an emergency fund not only ensures financial stability but also improves your mental health by reducing stress and anxiety about the unknown.

Just as important as preparing for the unexpected is aligning your finances with your faith and generosity.

Tithe and Practice Generosity to Strengthen Your Financial Health

You might not expect to see generosity on a list of money management tips, but biblical financial wisdom often turns worldly advice upside down. When we give, especially from our first fruits, we acknowledge that all we have comes from God.

Whether it’s a tithe (10% of your income) or other forms of giving, prioritising generosity strengthens your financial health and fosters a mindset of abundance.

The Bible reminds us of this reality:

"But this I say: He who sows sparingly will also reap sparingly, and he who sows bountifully will also reap bountifully" (2 Corinthians 9:6, NKJV).

Apart from reaping bountifully, aligning with God’s requirements prepares us for His promises, like His promises to rebuke the devourer for our sakes.

“And I will rebuke the devourer for your sakes, So that he will not destroy the fruit of your ground, Nor shall the vine fail to bear fruit for you in the field,” Says the Lord of hosts; “And all nations will call you blessed, For you will be a delightful land,” Says the Lord of hosts” (Malachi 3:11-12, NKJV).

Tithing isn’t about losing money; it’s about trusting God with your finances. And often, those who practice regular giving find themselves more disciplined and financially prepared for life.

But to give faithfully and save effectively, you must first guard against one of the biggest financial traps: debt.

Avoid Debt Traps and Credit Card Temptations

While credit cards and loans can be helpful tools, they can also lead to financial slavery if mismanaged.

In your first year on the job, it’s tempting to “treat yourself” or upgrade your lifestyle. But be cautious. Not all debt is bad, but high-interest debt can quickly erode your progress.

Stick to using credit only for planned, budgeted purchases—and always pay your balance in full. Avoid loans for wants, and never borrow money to impress others.

The Bible has a stern warning on debt:

"The rich rules over the poor, and the borrower is servant to the lender" (Proverbs 22:7, NKJV).

If you already have debt, make a plan to tackle it strategically. Start with the highest-interest balances first, and celebrate small victories along the way.

Once you’ve avoided the debt trap, you can start making confident strides toward your long-term financial goals.

Set Long-Term Financial Goals and Start Planning Early

It’s never too early to start planning for your financial future.

Whether your goal is to own a home, start a business, or retire comfortably, you need a clear plan and timeline to get there.

Begin by identifying your savings goals.

For example, how much do you want to have saved in 5 or 10 years? Then research how much you’ll need to contribute monthly to get there, considering potential interest from investments or retirement accounts.

Working with a financial advisor can also provide personalised guidance tailored to your income and aspirations. They can help you set realistic goals, understand investment options, and make wise financial decisions.

With your long-term plans in place, it’s essential to stay inspired and consistent. That’s where your mindset and motivation come into play.

Stay Motivated with Faith-Aligned Money Goals

Managing money well isn’t just about numbers. It’s also about mindset, motivation, and values. Align your financial goals with your faith, purpose, and calling.

For instance, do you want to save money so you can one day fund a ministry or help family members? Do you want to be debt-free so you can serve more freely? Write those motivations down. Keep them visible.

Your financial discipline is not just a personal achievement. It’s a spiritual journey. As you grow in your money management, you also grow in character, stewardship, and readiness to fulfill your God-given purpose.

Conclusion

Your first year on the job sets the tone for the rest of your financial life. With wise money advice, consistent habits, and a biblical foundation, you can be financially prepared for whatever the future holds. Don’t wait for a crisis or a higher salary to begin managing your money well.

Start now. Start small. Start smart.